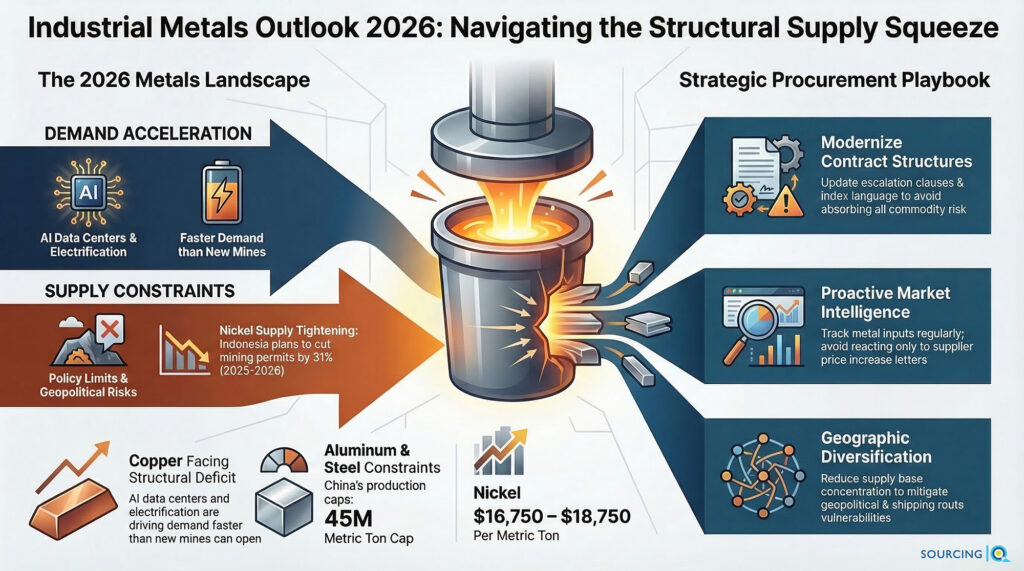

Industrial commodity markets are entering a volatile phase — and “volatile” is doing most of the heavy lifting in that sentence. This evolving industrial metals outlook for 2026 is directly impacting how manufacturers approach sourcing, supplier selection, and cost management.

This isn’t normal market noise. Copper, nickel, aluminum, and steel are all being shaped simultaneously by geopolitical disruption, structural demand from electrification and AI infrastructure buildout, and supply constraints that aren’t going away quickly. For manufacturers, these forces show up directly in margins, procurement planning, supplier negotiations, and long-term direct materials sourcing strategy.

The short version: near-term volatility and long-term structural demand growth are pulling in the same direction — up. Procurement teams that get ahead of this will be in a much better position than those reacting to it.

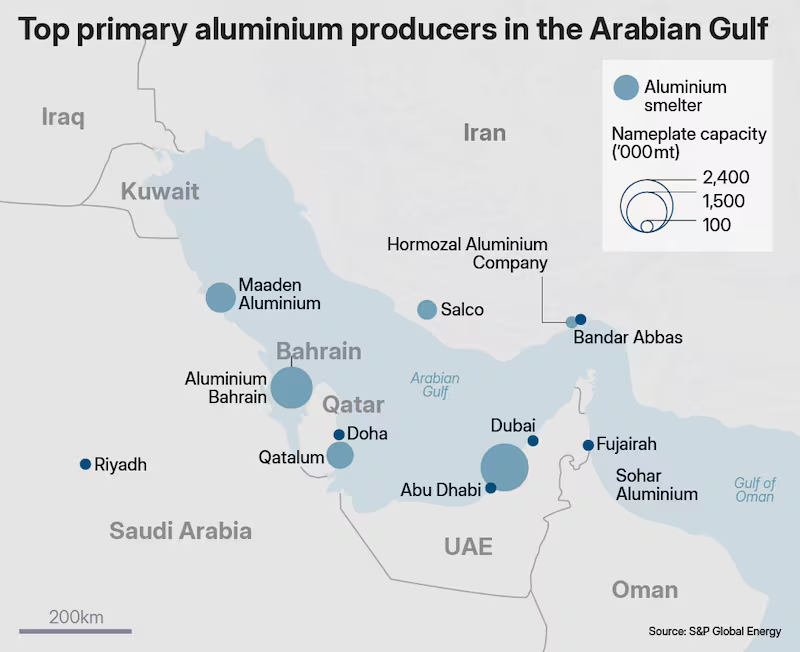

Approximately 21% of global aluminum production in 2025 originated in the Middle East. That supply is landlocked with the effective closure of Hormuz. Alba has declared force majeure and are shutting down 19% of their capacity in response. Qatalum announced a controlled shutdown in their Qatar facility, reducing production to around 60% capacity. Where possible, companies are shifting to land-bridges to Jeddah and Sohar to move product, however that has a significant impact to cost estimated at $45 to $60 per tonne in additional freight costs.

What Is the Industrial Metals Outlook for 2026?

The outlook for industrial metals in 2026 is defined by two forces competing for the same supply base: rising structural demand and constrained supply growth.

The demand side is being driven by:

- Rapid expansion of AI data centers, which require large quantities of copper and aluminum for power distribution

- Continued electrification of transportation and energy systems globally

- Government investment in renewable energy infrastructure

- Recovery and growth in industrial manufacturing activity

The supply side is being squeezed by:

- Policy-driven production limits in key producing countries

- Energy cost increases forcing smelter and refinery curtailments

- Mining disruptions from labor, environmental, and geopolitical sources

- Shipping route vulnerabilities that affect delivery timing and cost

The result is a market that may stay structurally tight for years — not just quarters. Commodity volatility has become one of the more persistent procurement challenges in manufacturing, particularly for mid-market industrial companies that don’t have the hedging infrastructure or buying power of large enterprises. Many companies in this position turn to procurement consulting for manufacturers to build more resilient sourcing strategies.

Here’s a breakdown of each key metal and the trends we’re keeping an eye on.

*All numbers are current as of March, 2026.

Copper: The Metal Everyone Is Watching

Copper remains the most closely watched industrial metal because it sits at the intersection of every major demand driver — AI infrastructure, electrification, EV production, and grid modernization.

Prices have recently traded near $5.90 per pound after periods of significant volatility driven by speculative activity and seasonal demand shifts in China around Lunar New Year. But the price swings shouldn’t distract from the underlying story: structural demand is growing faster than supply can reasonably keep up.

Here’s why the long-term outlook remains bullish:

AI infrastructure and data centers – Modern hyperscale data centers can require up to ten times the electrical load of traditional facilities. That electrical load requires copper — in power distribution, cooling systems, and connectivity. The AI buildout is a copper buildout.

Electrification – EVs, renewable generation, and upgraded electrical grids all require significantly more copper than legacy technologies. This demand isn’t speculative — it’s tied to infrastructure commitments that are already funded.

Limited new supply – New copper mine development takes years. Existing major mines are dealing with power shortages, environmental permitting constraints, labor disputes, and operational disruptions. Supply growth is not keeping pace with demand growth.

Some forecasts suggest the copper market could enter structural deficit conditions as early as 2026, with long-term demand potentially tripling by 2045. For manufacturers sourcing copper-intensive components, that’s not a background risk — it’s a planning input.

Nickel: Indonesia’s Policy Shift Changes the Equation

Nickel markets are undergoing a structural change driven largely by Indonesia, which dominates global production.

Recent price movement has placed nickel in the $16,750–$18,750 per metric ton range, reflecting anticipated supply tightening. The driver: Indonesia has announced plans to reduce mining permits from 379 million wet tons in 2025 to approximately 260 million tons in 2026 — a meaningful cut in potential global supply.

This comes while demand is simultaneously increasing from EV battery production, energy storage systems, stainless steel manufacturing, and AI data center infrastructure.

The implication for manufacturers: nickel-intensive categories may see pricing pressure that doesn’t ease quickly. Supplier diversification and contract structure — particularly around escalation clauses and index language — deserve close attention.

Aluminum: Quietly Tightening

Aluminum doesn’t generate the same headlines as copper, but the supply picture is tightening in ways that matter for manufacturers.

Three factors are converging:

China’s production cap – China, the world’s largest aluminum producer, is approaching its self-imposed ceiling of 45 million metric tons annually. That limits the ability of global supply to expand quickly from the world’s largest source.

Energy costs – Aluminum smelting is extremely energy intensive. Rising power costs in multiple regions are forcing producers to curtail output or close facilities. This isn’t a short-term issue — energy economics for smelters have structurally changed in many markets.

Renewable demand – Aluminum plays a significant role in solar panels, wind turbines, and electrical transmission infrastructure. The energy transition is both a supply constraint (energy-intensive production) and a demand driver (infrastructure components) simultaneously.

Manufacturers using aluminum in fabricated components, packaging, or structural applications should be reviewing supplier capacity commitments and contract protections now, not after the next price move.

Steel: Regional Divergence Is the Story

Steel markets aren’t moving in one direction — they’re moving in several, depending on geography.

United States – Domestic steel prices have shown modest upward momentum, supported by demand and the continued effect of Section 232 tariffs providing price support for domestic producers. For manufacturers sourcing domestically, the environment is manageable but not favorable.

China – Prices remain under pressure from weak property sector demand and government overcapacity controls. This creates potential import opportunities for some buyers, but with increasing trade policy risk attached.

India – India is rapidly scaling steelmaking capacity, with government plans targeting a 50 percent increase by 2030. This could meaningfully influence global supply dynamics — and create new sourcing options — over the next several years.

For multi-plant sourcing environments or manufacturers with global sourcing exposure, these regional differences create both risks and opportunities depending on how supply chains are structured.

Freight Markets: Seasonal Weakness, But Watch Hormuz

Shipping markets add another variable to the 2026 procurement picture.

The Baltic Dry Index recently declined across several consecutive sessions — typical seasonal behavior tied to Chinese New Year factory slowdowns. Container shipping shows mixed trends: Asia to US West Coast rates have moved modestly higher, while Asia to US East Coast rates have eased slightly.

The more significant risk sits in the Middle East. Recent military activity involving Iran has disrupted tanker movement through the Strait of Hormuz — the corridor responsible for roughly 20 percent of global oil supply. Sustained disruptions there can quickly cascade into higher bunker fuel prices, elevated shipping insurance premiums, and increased freight costs across global supply chains.

Freight cost volatility isn’t new — but it’s become a more permanent factor in total landed cost calculations than manufacturers accounted for three years ago.

What This Means for Procurement Teams

Commodity market intelligence used to be something large enterprises paid attention to and mid-market manufacturers ignored. That gap is closing — not because mid-market teams have more bandwidth, but because the margin exposure from commodity volatility is too significant to manage reactively.

A few practical implications:

Strengthen commodity monitoring – You don’t need a full market intelligence function — but someone should be tracking the metals and inputs most relevant to your categories on a regular cadence, not just when a supplier sends a price increase letter.

Review contract structures – Escalation clauses, index language, and surcharge definitions all become more important in volatile markets. If your contracts are silent on commodity movement, you’re absorbing all the risk.

Use structured sourcing events – Running competitive sourcing events using disciplined RFQ best practices for manufacturers can help mitigate cost increases and support direct materials cost reduction — but only if the events are structured for comparability. Informal quoting doesn’t create the same leverage. Teams that haven’t formalized their approach should understand how to run a direct materials RFQ before launching sourcing events.

Diversify where it matters – Geopolitical disruptions and supply shocks don’t hit all supplier bases equally. Manufacturers with geographic concentration in their supply base for critical materials are carrying more risk than they may realize.

Align with market cycles – Seasonal patterns in demand and shipping create pricing windows. Procurement teams that understand those patterns can time purchases and contract renewals more strategically than those reacting to them.

The Bottom Line

The industrial metals outlook for 2026 isn’t a “wait and see” situation for manufacturers. Copper, nickel, aluminum, and steel are all under structural demand pressure with constrained supply — and geopolitical disruption is adding a layer of volatility that purchasing teams can’t absorb through relationships and hustle.

Manufacturers that treat commodity exposure as a strategic sourcing problem — not just a finance problem — will be better positioned to protect margins, maintain supply continuity, and move faster when the market creates favorable windows.

Procurement isn’t a transactional function anymore. In a volatile commodity environment, it’s a competitive differentiator. Leading manufacturers are formalizing direct materials strategic sourcing capabilities to manage this complexity.

Questions About Industrial Metals

Why are industrial metals prices rising?

Industrial metals prices are rising due to structural demand from electrification, renewable energy infrastructure, and AI data center expansion combined with supply constraints in mining, smelting, and logistics.

Which metals are most important for manufacturers?

The most critical industrial metals for manufacturers include copper, aluminum, nickel, steel, and rare earth elements. These materials are essential for electrical systems, machinery, transportation equipment, and infrastructure.

How can manufacturers manage commodity price volatility?

Manufacturers can manage commodity volatility through strategic sourcing best practices including supplier diversification, structured RFQs, contract protections (escalation clauses, index language), long-term supply agreements where appropriate, and proactive market monitoring.