Nine weeks into what is now the largest energy supply disruption in recorded history, the question procurement teams are asking has changed.

It’s no longer “when does this normalize?”

It’s “what does our cost structure look like if it doesn’t?”

This week’s signals mark a turning point. Oil markets have effectively repriced Q3. Freight costs are resetting structurally ahead of peak season. Multiple commodity chains — from stainless steel to semiconductors — are converging toward near-term decision deadlines simultaneously.

Geopolitical risk is no longer theoretical. It is actively shaping price formation, logistics behavior, and supplier availability in real time. Procurement teams still operating in reactive mode are already behind.

What Changed in the Last Two Weeks

Three shifts have occurred that change the planning context:

- The market moved from volatility to repricing.

- Logistics costs are resetting structurally — not temporarily.

- Procurement timelines are compressing across multiple categories at the same time.

The cumulative result: procurement teams are no longer reacting to a disruption. They’re operating inside a new baseline.

Oil: The Week That Set the Floor for Q3

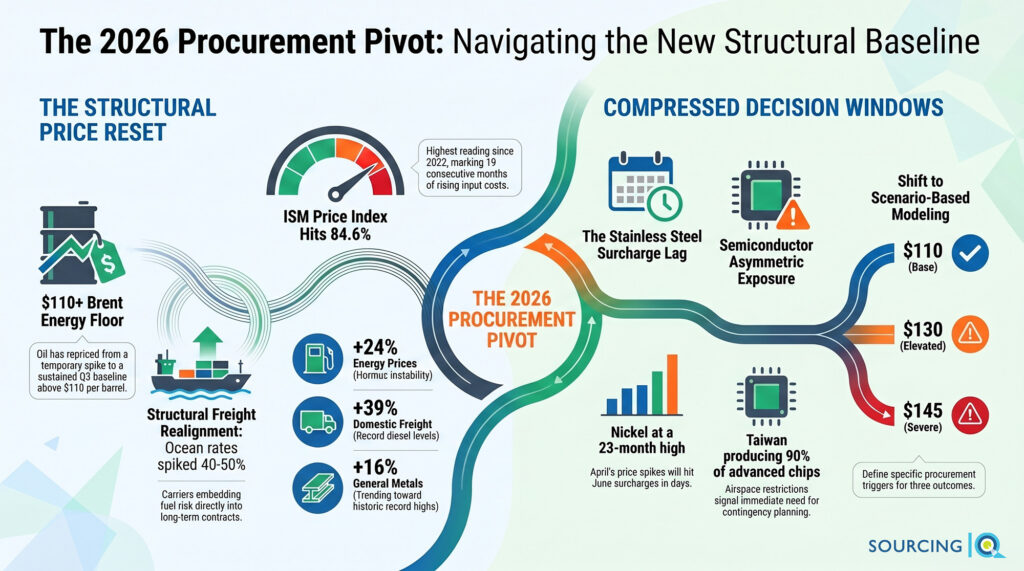

Brent crude spiked to $126.41 per barrel — a four-year high — before settling near $108 with extreme intra-week volatility. July futures, the actual planning benchmark, remain above $110.

That volatility isn’t noise. It’s the market pricing diplomatic uncertainty in real time.

The introduction of Project Freedom, a U.S. naval presence in the Strait of Hormuz, has created a genuine fork in the road:

Scenario 1 — Partial normalization: Commercial transit resumes. Freight surcharges begin easing. Energy markets stabilize at elevated levels.

Scenario 2 — Escalation: Hormuz closure resumes. Oil spikes back toward $125+. Polymer, freight, and metals costs reprice rapidly.

Early signals point toward continued instability. Iran engaged militarily following the Project Freedom announcement, which means Scenario 2 cannot be treated as a tail risk. It’s a live possibility with active precursors.

Where oil above $110 actually hits manufacturing costs:

Transportation: Diesel approaching record levels. Every truck move is more expensive than the February baseline.

Energy-intensive materials: Plastics, resins, and chemicals are repricing as feedstock costs rise in parallel with oil.

Freight surcharges: Carriers are embedding fuel risk directly into contracts. Logistics cost is becoming less predictable as a line item, not more.

Oil above $110 isn’t just a macro signal for manufacturers. It’s a simultaneous input cost reset across multiple categories.

Freight: Three Layers, One Structural Reset

Freight markets have stopped reacting to headlines. They’re resetting structurally — and the distinction matters for how procurement teams should plan.

Ocean freight: Transpacific rates are up approximately 40%. Transatlantic rates have spiked as much as 50% in recent weeks, with additional increases already scheduled for May. The constraint isn’t demand. It’s network disruption: vessels stranded, feeder networks impaired, transshipment hubs backlogged.

Air freight: The traditional escape valve is now constrained. Jet fuel costs have surged. Airlines are reducing capacity. Air freight premiums are significantly higher than most teams modeled.

Domestic freight: Diesel is up approximately 39% since the conflict began. Fuel surcharges are rising across carrier contracts. This affects every manufacturer, regardless of import exposure.

The timing signal that matters most right now: Peak season freight contracting is happening now. Teams waiting for normalization are making an implicit bet that freight will correct before peak demand layers on top of existing disruption. There is no evidence supporting that assumption.

Nickel & Stainless Steel: A Deadline Most Teams Missed

While attention has focused on oil and ocean freight, a quieter but more time-sensitive shift is playing out in nickel and stainless steel.

Nickel prices are at a 23-month high, approximately $19,450 per tonne, driven by Indonesian policy changes raising the structural cost base and supply disruptions tied to Middle East inputs.

The procurement-specific reality: stainless alloy surcharges lag commodity price movement by four to eight weeks. April price increases translate to June surcharge increases. For any manufacturer using 304 stainless, 316 stainless, or components sourced through process equipment, piping, or fastener supply chains — the action window is measured in days, not weeks.

This is one of those situations where knowing about the lag and not acting is functionally equivalent to not knowing.

The Bigger Pattern: Converging Decision Windows

This week’s signals aren’t isolated market movements. They’re converging toward compressed decision windows across multiple categories simultaneously:

- Oil → Q3 cost baseline needs to be established now

- Freight → May contract cycle is active

- Stainless → June surcharge window closes soon

- China/Taiwan → immediate geopolitical signal with direct semiconductor implications

This creates a new operating condition: procurement timing is becoming as important as procurement strategy. The best analysis in the world doesn’t create value if the decision comes after the window closes.

China/Taiwan: The Next Signal to Watch

The China/Taiwan airspace restriction expires this week. This is not a routine event.

Taiwan produces approximately 90% of advanced semiconductors. Current restrictions indicate a sustained military readiness posture. A Trump-Xi meeting follows within days.

The near-term risk isn’t immediate disruption — it’s asymmetric exposure. If escalation occurs, the impact would be rapid, severe, and difficult to mitigate after the fact. Semiconductor-dependent manufacturers should have contingency thinking in place before the expiration, not as a response to it.

The Data Is Confirming the Shift

April ISM data reinforces what procurement teams are already experiencing operationally:

- Prices Index at 84.6% — the highest reading since 2022

- 19 consecutive months of rising input costs

- Lead times still elevated

- Labor constraints unresolved

This isn’t a temporary spike. It’s a sustained repricing environment with multiple reinforcing inputs.

The World Bank’s latest commodity outlook adds the macro layer: energy prices up 24%, overall commodities up 16%, fertilizers up 31%, metals trending toward record highs. Procurement exposure is no longer isolated to one or two categories — it’s spreading across interconnected commodity systems simultaneously.

What Procurement Teams Should Be Doing This Week

This is not a monitor-and-wait environment. The teams performing best right now are acting across three areas:

- Extend the planning horizon to Q3. Weekly reaction cycles are insufficient. You need forward pricing assumptions, scenario-based planning, and cost exposure modeling that accounts for multiple outcomes — not just the one that looks most likely today.

- Lock critical positions where timing windows are closing. Freight contracts before peak season pricing layers on. Stainless before June surcharges land. Energy-linked categories before further escalation changes the cost structure.

- Build scenario-based decision frameworks — not predictions. Model base case ($110 Brent), elevated case ($130), and severe case ($145+). Then define the specific procurement actions triggered by each scenario. The goal isn’t to predict which scenario materializes. It’s to remove the lag between “conditions changed” and “we responded.”

The Bottom Line: This Is the New Baseline

The biggest mistake procurement teams can make right now is treating this as a temporary disruption waiting to resolve itself.

Freight is resetting. Energy is repricing. Commodity chains are cascading. Decision windows are compressing.

This is a structural shift — and procurement performance over the next two quarters will be defined by how quickly teams adapt to operating inside it, rather than waiting for conditions to return to normal.

The market has already moved. Now execution is the gap.