Manufacturing procurement hasn’t returned to “normal.” The acute shocks of the early 2020s may have cooled, but the pressure on procurement hasn’t.

In 2026 and beyond, procurement leaders are operating in a permanently higher-stakes environment: supply instability that never fully disappears, inflationary residue baked into cost structures, margin compression that makes every percentage point matter, private equity expectations that demand speed and proof, and multi-plant complexity that turns “simple sourcing” into a coordination problem.

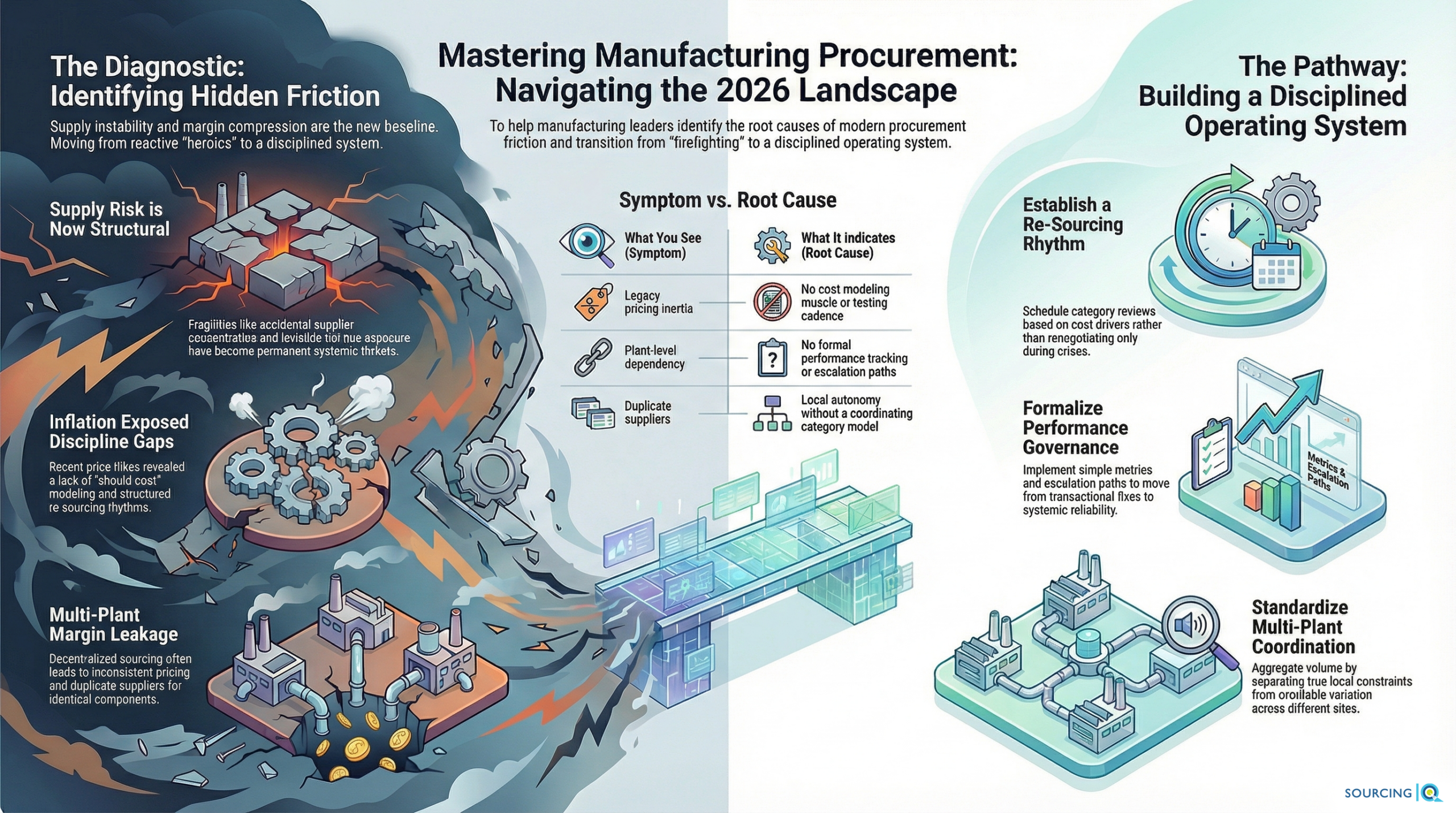

We don’t expect these to be mere “trends” that come and go. What follows is a diagnostic view of the most common procurement challenges manufacturers are facing right now—what’s really behind them, why they persist, and what practical corrective pathways tend to work.

Supply Risk Is No Longer Episodic

Supply risk used to feel event-driven: a port disruption, a natural disaster, a geopolitical flare-up. Now it feels continuous—not because every day is a crisis, but because the system has more embedded fragility.

What you’re seeing:

- Heavy dependence on a small number of suppliers (often without meaning to)

- Geographic clustering (too much critical supply in one region)

- Tier-two exposure that nobody can see until it bites

- Long-standing suppliers that haven’t been stress-tested under modern constraints

What it usually indicates:

- Accidental concentration. Single sourcing isn’t always a decision; sometimes it’s just what happens over time.

- Visibility gaps. Without consolidated spend and category clarity, risk hides in plain sight.

- No intentional supplier strategy. The supply base grew organically, not deliberately.

Corrective pathways:

- Make supplier concentration a managed choice: where you’re intentionally single-source, treat it like a risk position with mitigation.

- Use spend visibility to find “hidden” dependency (category + supplier concentration patterns).

- Tie supplier strategy to realities like qualification barriers and capacity—not preference.

This is where supply chain design impacts sourcing outcomes becomes unavoidable. If your footprint, logistics model, and supplier geography are mismatched, procurement ends up compensating with expedites and heroics instead of decisions.

Inflation Isn’t the Core Problem Anymore

Inflation dominated procurement conversations for years. But inflation itself isn’t the main issue now.

Inflation exposed weak sourcing disciplines.

What you’re seeing:

- Cost increases accepted with limited structured validation

- “We had no choice” becoming the default narrative

- Legacy pricing inertia—prices that never come back down

- Negotiations that reset nothing because there’s no benchmark

What it usually indicates:

- No cost modeling muscle (even lightweight “should-cost” thinking)

- No structured re-sourcing cadence (categories go years untested)

- Weak RFQ discipline (poor comparability, unclear scope, no follow-through)

- Category ownership that’s functional but not strategic (someone buys it ≠ someone manages it)

Corrective pathways:

- Build a re-sourcing rhythm by category—so you’re not renegotiating only when you’re angry.

- Use cost-driver thinking as an anchor (material, labor content, yield, freight, tooling assumptions).

- Treat RFQs as an execution discipline, not an email chain.

Supplier Reliability Is Becoming a Performance Differentiator

Price is not the only measure of supplier value anymore. In a world of tight labor, tight capacity, and persistent disruption, supplier reliability is often the difference between predictable operations and recurring firefighting.

What you’re seeing:

- On-time delivery variability creeping up

- Quality issues that create rework and schedule disruption

- Responsiveness depending on who knows whom

- Performance problems handled transactionally (“call them again”) instead of systemically

What it usually indicates:

- No formal performance tracking (OTD, defects, response time)

- Plant-level relationship dependency (performance is “managed” by personal rapport)

- No escalation structure or consequences (everything is urgent, nothing is accountable)

- Procurement and operations misaligned on what “good” looks like

Corrective pathways:

- Define a simple performance cadence (monthly for critical suppliers, quarterly for stable ones).

- Use a few metrics that actually matter and act on them consistently.

- Build an escalation path that doesn’t rely on emotion or relationship capital.

This is exactly where a supplier performance improvement plan becomes a practical next step—because reliability isn’t a speech. It’s a system: metrics, cadence, escalation, and consequence.

Fragmented Multi-Plant Sourcing Structures

Multi-plant complexity is one of the most underestimated procurement challenges in manufacturing. It’s also one of the easiest ways to leak margin quietly.

What you’re seeing:

- Duplicate suppliers across sites for similar components

- Inconsistent pricing for functionally identical items

- Decentralized RFQs that create noise, not leverage

- Missed opportunities to aggregate volume and standardize specs/terms

What it usually indicates:

- Local autonomy without a coordinating model

- No category strategy that spans plants

- Different requirements that may be real—or may just be inherited preferences

- Lack of a consolidated “award + implement” muscle across sites

Corrective pathways:

- Separate what must stay local (true constraints) from what can be standardized (avoidable variation).

- Create a category view across plants—then decide where aggregation makes sense.

- Build a multi-plant RFQ approach that prioritizes comparability and implementation, not bureaucracy.

This section should naturally bridge into later consolidation and supplier strategy posts—but the diagnostic point is simpler: fragmentation is rarely intentional, and it is almost always expensive.

Procurement Teams Are Under-Tooled and Under-Structured

Mid-market procurement teams are often lean by design. The problem is that the mandate has expanded faster than the structure supporting it.

What you’re seeing:

- Procurement asked to manage cost, risk, performance, and integration—simultaneously

- Email-based RFQs still common

- Limited analytics capability (data exists, but insight doesn’t scale)

- Tribal knowledge and heroics substituting for playbooks

What it usually indicates:

- The team isn’t lacking talent—it’s lacking repeatable frameworks.

- Work is being prioritized by urgency, not impact.

- Procurement becomes a firefighter role, which crowds out strategic work.

Corrective pathways

- Standardize the few workflows that create repeatable value: category strategy, RFQ execution, supplier performance management, governance.

- Build “minimum viable” templates and routines that reduce reinvention.

- Treat capability building as a throughput multiplier—not overhead.

This is where procurement consulting for manufacturers can be positioned as surge capacity + operating system design, not “extra hands.” The goal isn’t dependency. The goal is a team that can execute with discipline when the consultants are gone.

The Real Issue: Inconsistent Sourcing Discipline

Across all of these challenges—supply risk, inflation residue, supplier reliability, multi-plant fragmentation, lean teams—a common thread shows up:

The root cause is rarely external. The main culprit is inconsistent sourcing discipline.

When procurement operates without:

- clear category strategies

- structured RFQ processes built for comparability

- defined supplier performance management

- consolidated spend visibility

- governance around awards and compliance

…problems accumulate gradually:

- cost drifts upward

- risk becomes invisible until it’s urgent

- performance variability increases

- “exceptions” become the operating model

Many organizations treat issues as isolated events: renegotiate one supplier, address one quality flare-up, run one consolidation push. Without an underlying operating model, improvements don’t scale—and they don’t stick.

The manufacturers that perform best in 2026 and beyond won’t necessarily have the largest teams. They’ll have the most consistent structure.

Looking Ahead: What Will Define Strong Procurement Functions

2026 and beyond will reward procurement organizations that can operate deliberately under pressure.

Not perfectly. Not with zero disruptions. But with systems that prevent every problem from becoming a crisis.

Strong procurement functions will double down on:

- structured sourcing discipline (not ad hoc buying)

- performance governance (metrics + cadence + escalation)

- data-driven opportunity assessment (not dashboard theater)

- repeatable RFQ execution (comparability + follow-through)

- multi-plant coordination models that preserve local reality without losing leverage

- capability elevation as an ongoing practice

External pressures will continue. Markets will shift. Supply chains will remain complex.

The differentiator won’t be the absence of challenges. It will be the presence of a disciplined procurement operating system.