Procurement synergies show up in almost every manufacturing roll-up thesis. Aggregate the purchasing volume, consolidate the supplier base, capture the savings. It sounds clean on a deal model.

The reality is messier and far more conditional.

Some roll-ups generate meaningful procurement savings quickly, with relatively little execution effort. Others see minimal impact despite significant integration work and sincere intent. The difference isn’t ambition or resources. It’s structure — specifically, whether the conditions that make procurement synergies possible actually exist in the portfolio.

Before building synergy assumptions into a value creation plan, operating partners and deal teams should understand what those conditions are. And just as importantly, what happens when they’re not present.

If Portfolio Companies Buy the Same Categories — Synergies Become Real

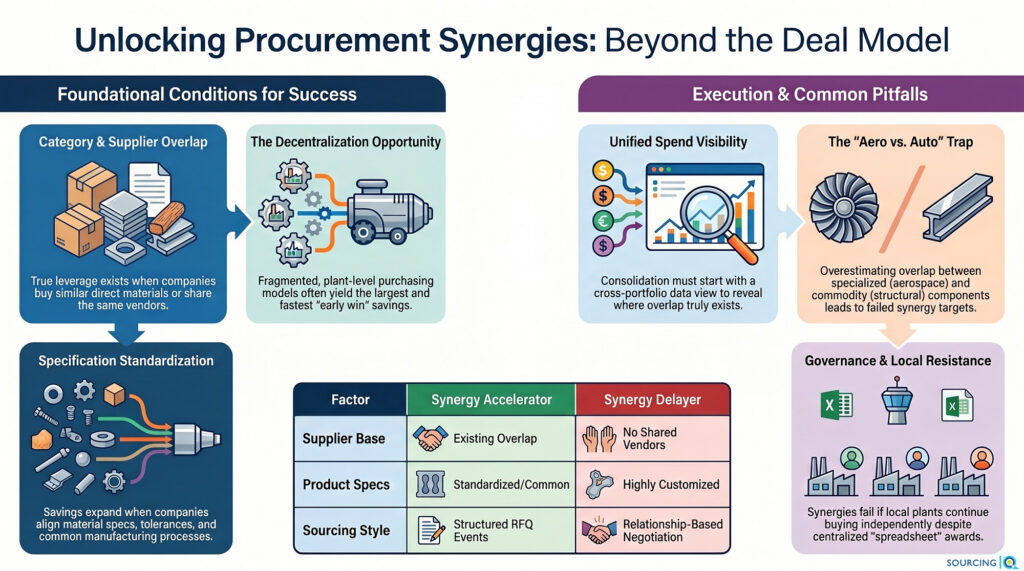

The most reliable foundation for procurement synergies is category overlap. When multiple portfolio companies are purchasing similar direct materials — machined components, castings, fabricated assemblies, resins, electronics — the basic math of aggregation works in your favor.

What becomes possible when category overlap exists:

- Total purchasing volume increases meaningfully when viewed as a single enterprise

- Supplier competition for that larger volume creates pricing leverage that didn’t exist when companies were buying separately

- Category-level sourcing strategies become viable — you can run a real event, not just a renegotiation

- Pricing structures, terms, and contract language can be standardized across companies

A roll-up of industrial manufacturers might reveal, for instance, that three portfolio companies are independently sourcing similar machined aluminum components from different regional suppliers — each negotiating as a small customer. Viewed collectively, that’s a different conversation with the supply base.

When category overlap is genuine, synergies aren’t theoretical. They’re better math waiting to be executed.

Consolidation creates sourcing opportunities—but only if they’re identified and executed. Let’s evaluate the potential across your portfolio.

If Suppliers Already Overlap Across Companies — Leverage Increases Further

Category overlap tells you what’s possible. Supplier overlap tells you how fast you can get there.

When multiple portfolio companies are already working with the same suppliers — even informally — procurement synergies can be captured with less disruption. The supplier relationship exists. What changes is the commercial position.

If multiple companies are dealing with the same vendor:

- Pricing differences across companies can be identified and closed quickly

- Volume commitments can be consolidated into a single, more favorable agreement

- Contract terms — payment, freight, indexing, minimums — can be standardized

- The relationship elevates from “local preferred vendor” to “strategic supplier” with performance expectations to match

When supplier bases don’t overlap, the path is longer. Procurement teams have to either work with each company’s existing suppliers separately or evaluate new alternatives — which introduces switching costs, qualification timelines, and operational risk that can delay or dilute the synergy.

Supplier overlap is a multiplier on execution speed. It’s worth assessing explicitly during due diligence, not discovered during integration.

If Sourcing Is Decentralized Pre-Acquisition — The Opportunity Is Often the Largest

Most manufacturing businesses that enter PE ownership are buying in a decentralized model. Individual plants manage their own supplier relationships, negotiate independently, and make purchasing decisions based on local priorities. Nobody has a cross-plant view. Nobody is aggregating.

This structure reliably produces:

- Supplier fragmentation — more vendors than the volume justifies

- Inconsistent pricing — the same part at different prices in different plants

- Duplicated relationships — the same supplier appearing three times under three different names

- Zero enterprise leverage — the business is buying like it’s ten small customers instead of one

For procurement synergy capture, this is actually the most favorable condition. The opportunity is large precisely because nobody has organized around it yet. Once spend data is consolidated and analyzed at the enterprise level, the inefficiencies surface quickly — and early wins are accessible without complex execution.

Decentralization is often the clearest signal that meaningful procurement synergies exist. The gap between current state and possible state is just waiting to be closed.

If Specifications Can Be Standardized — Synergies Expand

Category overlap opens the door. Spec standardization determines how wide it opens.

When portfolio companies are buying components that can be aligned — shared material specs, compatible tolerances, common manufacturing processes — procurement can aggregate demand more effectively across the group. Larger sourcing events. Simpler supplier bases. More consistent pricing.

When products are highly customized or engineered differently across companies, standardization becomes constrained. You may be in the same general category — say, machined components — but if one company’s parts require specialized processes that another’s don’t, aggregation is limited to the portions that overlap.

The practical implication: don’t assume category similarity means specification compatibility. It often does. But the delta between “similar” and “identical” is where synergy assumptions get stress-tested in execution.

If Portfolio Companies Operate in Different Supply Chains — Synergies May Be Minimal

This is the part that gets glossed over in deal memos.

Not all roll-ups produce meaningful procurement synergies. If portfolio companies are in genuinely different industries — different materials, different supply chains, different supplier markets — category overlap may be minimal regardless of how the investment thesis reads.

A company sourcing complex electronics assemblies and a company sourcing structural steel fabrications may both be “industrial manufacturers.” They’re not buying from the same supply base, and aggregating their volumes doesn’t create leverage for either of them.

In these situations, procurement value creation is still possible — it just comes from a different source. Process improvement, not consolidation:

- Improving sourcing discipline within each company independently

- Building spend visibility that didn’t exist before

- Standardizing procurement processes across the portfolio even when categories don’t overlap

- Elevating procurement capability so each company sources better on its own

That’s real value. It’s just not the synergy assumption that typically shows up in the model.

Why Procurement Synergies Often Fall Short

When roll-up procurement synergies underperform, the causes are usually predictable:

Overestimated category overlap at the deal stage. “Both companies buy machined components” sounds like overlap. If one buys precision aerospace-grade components and the other buys commodity structural brackets, the supplier base won’t converge.

Underestimated execution complexity. Supplier transitions require qualification, tooling, engineering alignment, and operational continuity planning. When integration teams underestimate this, savings get delayed — or never fully captured.

Limited spend visibility post-close. If nobody consolidates procurement data quickly, the opportunity identification phase takes months instead of weeks. By the time the analysis is done, early momentum is gone.

Resistance from plant-level teams. Plants that have managed their own sourcing for years don’t naturally yield to enterprise procurement decisions. Without governance and change management, local teams continue buying the old way — and the “centralized” strategy exists only on paper.

Lack of structured sourcing execution. Synergies don’t get captured by identifying them. They get captured by running disciplined sourcing events, implementing awards, and making the savings stick through governance and compliance.

How Procurement Synergies Are Actually Captured

The organizations that successfully realize procurement synergies in roll-ups tend to follow a consistent pattern:

They start with spend visibility across portfolio companies — not just within each company, but a consolidated view that reveals where overlap exists and where it doesn’t. This prevents wasted effort on categories that won’t produce synergies.

They prioritize based on overlap quality, not just volume: categories where specifications are comparable, supplier capabilities align, and volume can be aggregated without significant operational disruption.

They run structured sourcing events — disciplined RFQs that create genuine comparability and competitive tension — rather than relying on relationship-based renegotiations that tend to produce polite discounts rather than structural improvement.

They build governance to make sourcing decisions stick across plants and companies, because synergies that live only in awards and not in actual purchasing behavior aren’t synergies — they’re spreadsheet entries.

None of this is fast. Sequencing and discipline matter. But when the foundational conditions exist and execution follows, procurement synergies in manufacturing roll-ups are among the most reliable value creation levers available.

Procurement Synergies Are Earned, Not Assumed

The investment thesis that says “we’ll get cost savings through procurement” isn’t wrong. It’s just incomplete.

Procurement synergies in manufacturing roll-ups depend on category overlap, supplier alignment, specification comparability, sourcing structure, and execution discipline. When those elements align, the value creation is real and repeatable. When they don’t, expected savings won’t materialize — regardless of how confident the deal model looks.

The productive question isn’t “will we get procurement synergies?” It’s “what conditions would make them possible, and do those conditions exist in this portfolio?”

Because in manufacturing sourcing, leverage isn’t created by scale alone. It’s created by structure. Scale is just what makes the structure worth building.