If last month’s takeaway was that industrial metals markets were tightening, this month’s signal is more urgent:

The disruption has moved downstream, and it’s accelerating.

What started as a geopolitical and energy story centered on the Strait of Hormuz is now showing up in plastics, semiconductors, and fabricated materials, with real cost implications already hitting procurement teams in manufacturing.

This isn’t a continuation of the same trend. It’s an escalation.

And for manufacturers, the risk profile just expanded.

Summary: What Changed in the Industrial Supply Chain in April 2026?

The April 2026 supply chain update showed that disruption is no longer limited to industrial metals. Key developments include:

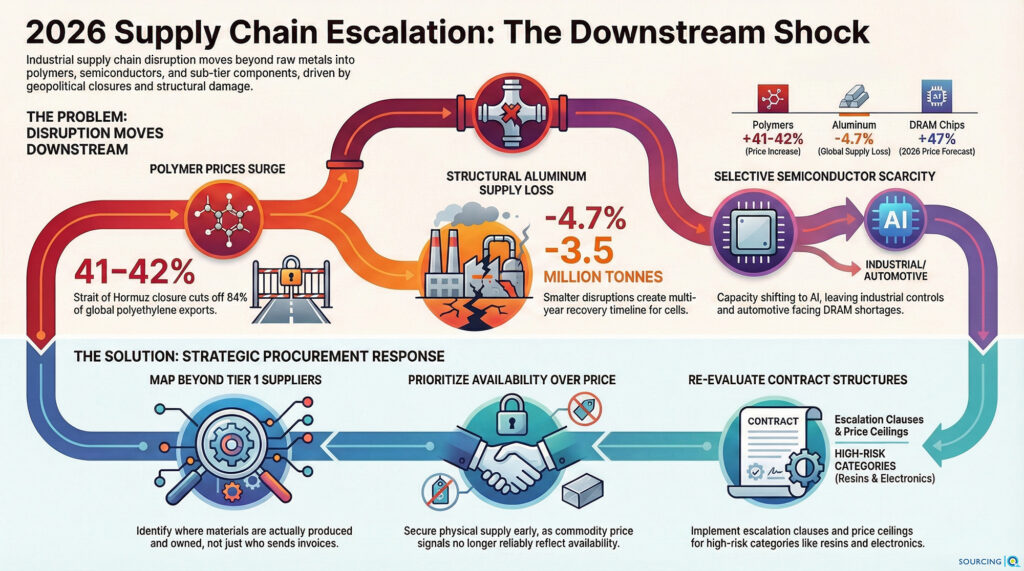

- Polymer prices rising over 40% due to Hormuz-related supply constraints

- Aluminum supply reduced by nearly 5% following smelter disruptions

- Semiconductor shortages shifting toward memory and AI-driven capacity constraints

- Supplier delivery times slowing across all major manufacturing sectors

For manufacturers, this means supply risk is moving beyond raw materials and deeper into components and sub-tier inputs.

What Changed Since the Last Outlook

Las month, we outlined how metals like copper, nickel, and aluminum were entering a structurally tight direct materials market driven by electrification, AI infrastructure, and supply constraints.

Just two weeks later, the picture shifted in three important ways:

- The disruption is no longer confined to metals

- Physical supply not (just price) is becoming the constraint

- The impact is now visible in real operating data

The March ISM Manufacturing PMI confirms this shift.

- Prices Paid: 78.3% (highest since June 2022)

- Supplier Deliveries: slowing across every major industry

- Zero commodities reported down in price

On paper, manufacturing still looks stable. In practice, input conditions are deteriorating rapidly.

Polymers: The Supply Shock Most Teams Haven’t Mapped Yet

The biggest development this week isn’t copper or steel.

It’s plastics.

The Strait of Hormuz disruption, initially framed as an oil and freight issue, has now fully translated into a global polymer supply shock.

Here’s the mechanism:

- The Middle East controls 84% of globally traded polyethylene exports

- Massive volumes of methanol and ethylene glycol (key resin inputs) flow through Hormuz

- When the strait closed, the feedstock supply chain effectively closed with it

The result:

- Polymer prices (PE, PP, PS) up ~41–42% since late February

- Naphtha (key feedstock) up ~74%

- Some packaging inputs up as much as 80%

This is where many procurement teams are exposed without realizing it.

Plastics, resins, and petrochemical derivatives are embedded across thousands of SKUs, from packaging to components to subassemblies.

And the situation just worsened.

Recent strikes on Iran’s Mahshahr petrochemical complex — a site producing 72 million tonnes annually — have taken supply offline in a way that won’t recover quickly.

This is no longer just a logistics issue.

It’s now a production destruction problem.

A Two-Tier Supply Chain Is Emerging

One of the most important and underreported developments this week is the emergence of a two-tier global supply system.

Iran has partially reopened the Strait of Hormuz — but only to “friendly” nations.

Countries like China and India have resumed access.

Western-aligned supply chains have not.

This creates a structural imbalance:

- Global benchmarks (like oil) may stabilize or fall

- But Western buyers still face constrained physical supply

We’re already seeing this divergence:

- Brent crude has declined

- Polymer prices continue rising

For procurement teams, this breaks a common assumption:

Commodity price signals no longer reliably reflect supply availability.

Aluminum: From Tight Market to Supply Shock

Aluminum has moved from a tightening market into something much more severe.

Recent strikes hit two of the world’s largest smelters:

- Emirates Global Aluminium (UAE)

- Aluminum Bahrain (Alba)

Combined with existing curtailments, the impact is significant:

- ~3.5 million tonnes removed from global supply (~4.7%)

But the more important detail is operational:

When aluminum smelters lose power, molten metal solidifies inside production cells.

Those cells don’t restart — they must be rebuilt.

That turns a disruption into a multi-year supply constraint.

For U.S. manufacturers (who already import ~60% of their aluminum) this introduces a second pricing pressure on top of tariffs:

- Physical supply loss

- Structural import dependency

Semiconductors: The Shortage Didn’t End — It Shifted

Another critical shift this week is in semiconductors — specifically memory.

The prevailing narrative was that the chip shortage had eased.

That is no longer accurate.

Key developments:

- Memory components now listed as both “up in price” and “in short supply”

- DRAM prices forecasted to rise ~47% in 2026

- Major producers reallocating capacity to AI-related chips

This is a classic zero-sum constraint:

Every wafer used for AI infrastructure is a wafer not available for:

- industrial controls

- automotive electronics

- factory automation

For manufacturers, this means:

The risk isn’t broad semiconductor shortage — it’s selective scarcity in critical components.

The Bigger Pattern: Supply Risk Is Moving Down the BOM

One of the most important strategic insights from this week’s data is this:

The highest risk is no longer at Tier 1 suppliers.

It’s deeper in the bill of materials.

Examples:

- commodity resins embedded in packaging

- standard semiconductors (MOSFETs, memory)

- aluminum in fabricated components

- low-cost parts with concentrated geopolitical exposure

As highlighted in the Nexperia case:

Small, low-cost components can create outsized production risk when supply is disrupted.

Most mid-market procurement teams are not systematically mapping this level of exposure.

What Procurement Teams Should Be Doing Right Now

This is not a “monitor and wait” environment.

The companies responding effectively are already acting on four fronts:

1. Mapping exposure beyond Tier 1

Understanding where materials are actually produced, processed, and owned — not just who invoices you.

2. Running structured sourcing events (RFQs) early

Teams that moved early are already securing domestic or alternative supply.

Those waiting for price increases are entering a tighter market. This is where direct materials cost reduction becomes critical.

Teams that haven’t formalized their approach should understand how to run a direct materials RFQ.

3. Re-evaluating contract structures

Escalation clauses, index alignment, and price ceilings are now critical, especially in:

- polymers

- aluminum

- electronics

4. Prioritizing physical availability over price signals

In multiple categories, availability — not cost — is becoming the constraint.

This changes sourcing strategy entirely.

The Bottom Line: This Is a Second-Order Shock

The first phase of this disruption was visible:

- metals tightening

- freight volatility

- geopolitical tension

The second phase is harder to see — but more dangerous:

- downstream material shortages

- embedded supply chain exposure

- divergence between price signals and availability

This is where procurement performance starts to separate.

Manufacturers that treat sourcing as a strategic function and act before disruptions fully materialize, will be in a fundamentally different position than those reacting to supplier price increases after the fact.