For the past several months, procurement teams have been fixated on a single question:

What happens next in the Strait of Hormuz?

It’s a fair question. The conflict has disrupted energy markets, freight routes, commodity pricing, and supplier planning across multiple industries.

But fifteen weeks into the disruption, some of the most important procurement signals have little to do with whether a diplomatic breakthrough happens tomorrow. As the latest SourcingIQ intelligence indicates, manufacturers are increasingly being squeezed by forces running on entirely different clocks: container rates, tariff deadlines, copper shortages, and persistent supplier inflation.

In other words: The next bottlenecks may not be where your team is looking.

Manufacturing Is Expanding — But Conditions Are Getting Harder

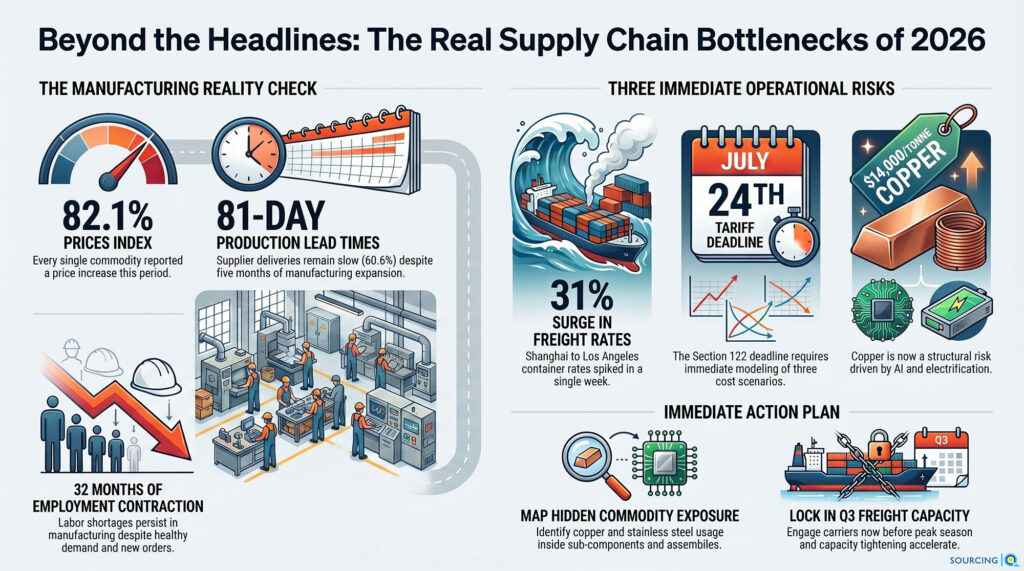

At first glance, the latest manufacturing data looks encouraging. The ISM Manufacturing PMI reached 54%, its highest reading since 2022 and the fifth consecutive month of expansion. New orders, production, and backlogs all remain positive.

However, procurement leaders should pay more attention to the subindexes than the headline.

Several warning signs continue to intensify:

- Prices Index: 82.1%

- Supplier Deliveries: 60.6%

- Production Materials Lead Time: 81 days

- Employment contraction for 32 consecutive months

- Zero commodities reported down in price

This creates an unusual environment. Demand remains healthy but supply conditions do not. That distinction matters because many organizations are treating economic expansion as a sign that conditions are improving when, operationally, sourcing teams are experiencing the opposite.

Container Rates Just Delivered a Warning Shot

The most immediate procurement signal this week may be freight. Container rates posted one of the largest single-week increases seen in years.

According to Drewry:

- World Container Index up 23%

- Shanghai to Los Angeles up 31%

- Shanghai to New York up 20%

- Asia to Rotterdam up 25%

What makes this development notable is that it isn’t being driven primarily by Hormuz. Three separate forces are stacking simultaneously:

- Peak Season Arrived Early

Carriers and logistics providers now report that the traditional August–October shipping peak effectively started in June.

- Tariff Deadlines Are Pulling Demand Forward

The July 24 Section 122 deadline is encouraging importers to accelerate shipments while they still have clarity on cost structures.

- Capacity Is Tightening

With fewer blank sailings and stronger booking activity, freight markets are tightening faster than many procurement teams anticipated.

The result is a market where companies that delayed freight decisions are now competing directly against companies that accelerated them.

The July 24 Tariff Clock Is Getting Ignored

One of the more surprising findings from conversations across the industry is how few procurement teams have modeled multiple outcomes for Section 122. Yet the deadline is less than two months away.

There are three realistic scenarios:

Scenario 1: Extension

Current tariff structures remain largely intact.

Scenario 2: Expiration

Some categories experience meaningful cost reductions as rates revert toward MFN levels.

Scenario 3: Targeted Expansion

Section 232 and Section 301 protections expand into additional sectors.

The key issue is not predicting which outcome occurs rather being prepared for all three. Many organizations have detailed supplier strategies but no documented tariff contingency plan. That gap becomes more expensive with every week that passes.

Copper Has Become a Strategic Procurement Issue

While nickel and stainless steel have received significant attention this year, copper may be emerging as the more important long-term story. Copper recently surpassed $14,000 per tonne and is now roughly 65% above early 2025 levels.

The drivers are increasingly structural:

- AI data center construction

- Section 232 copper tariffs

- Middle East supply disruptions

- Sulphur shortages affecting mining operations

- Ongoing electrification demand

For many manufacturers, copper exposure remains hidden because it appears inside components rather than as a purchased commodity.

Examples include:

- wire harnesses

- motors

- transformers

- connectors

- heat exchangers

- printed circuit boards

That creates a common blind spot. Organizations may believe they have limited copper exposure while their suppliers are quietly absorbing substantial copper cost increases.

Eventually those costs surface somewhere:

- supplier price increase requests

- quality reductions

- longer lead times

- supplier distress

The best time to understand your copper exposure is before that conversation happens.

AI Procurement Tools: The Mid-Market Gap Is Real

One of the more interesting themes emerging from recent procurement technology conferences is how differently enterprise and mid-market organizations experience the AI conversation.

Most AI procurement platforms are built around assumptions that simply don’t exist inside many manufacturing organizations:

- dedicated procurement technology teams

- large IT departments

- highly structured ERP data

- hundreds of millions in spend

For many mid-market manufacturers, the main challenge is identifying where AI actually creates practical value.

The highest-return opportunities currently tend to be:

- spend analytics

- supplier risk monitoring

- contract review

- RFQ automation

The lesson is simple: Don’t buy enterprise solutions designed for companies ten times your size. Solve the highest-friction procurement problem you have today.

What Procurement Teams Should Do Right Now

The common thread running through all of these signals is timing.

Container rates are rising now.

Tariff decisions arrive in July.

Copper costs are already moving.

Supplier lead times remain elevated.

The teams that perform best in this environment are focusing on four priorities:

- Revisit Q3 Freight Exposure

If significant ocean freight remains uncontracted, now is the time to engage carriers and forwarders.

- Model All Three Tariff Scenarios

Treat Section 122 as a planning exercise rather than a political forecast.

- Map Commodity Exposure Beyond Raw Materials

Copper, stainless, semiconductors, and other inputs often sit inside purchased components rather than direct material categories.

- Evaluate Procurement Technology Pragmatically

Focus on tools that solve immediate problems and generate measurable payback at your actual spend level.

The Bottom Line

The procurement risks that matter most this summer may not be the ones generating the biggest headlines. Container rates are rising faster than expected. Tariff uncertainty is approaching a hard deadline. Copper is behaving like a structurally constrained material rather than a cyclical commodity. Supplier lead times remain stubbornly elevated despite economic expansion. And procurement technology is evolving rapidly while much of the mid-market remains underserved.

The lesson from the latest signals is straightforward: Don’t let geopolitical headlines distract your team from operational realities.

The companies that outperform over the next six months will be the ones managing all of these signals simultaneously, not waiting for a single event to resolve before taking action.