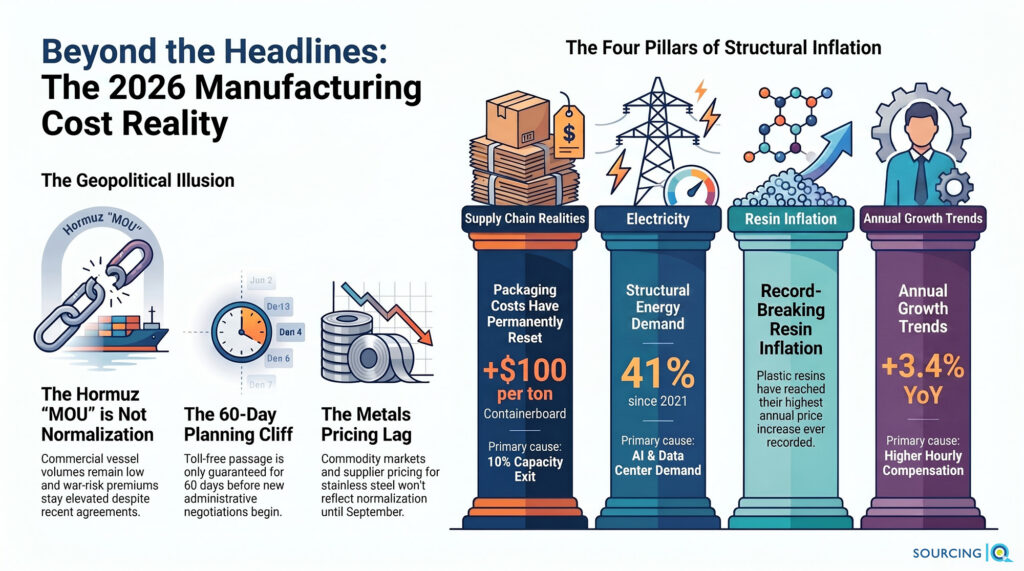

The Strait of Hormuz is reopening. Procurement teams should be relieved! They should also be careful.

After nearly four months of disruption, the United States and Iran signed a memorandum of understanding. Commercial vessels are moving again. More than twenty ships passed through the Strait on the first Saturday after the agreement, the highest single-day count since March. That’s real progress, and it matters.

Here’s the problem: the Strait is reopening, but your cost structure isn’t.

Most of the inflation now baked into manufacturing supply chains has nothing to do with Hormuz. Packaging costs are rising because capacity left the market permanently. Labor costs keep climbing. Electricity prices are moving up on structural demand growth that has nothing to do with oil tankers. Plastic resins are posting record inflation. The visible crisis is easing. The structural inflation underneath it is not — and treating those as the same problem is how procurement budgets get blindsided in Q3.

The Packaging Cost Reset Nobody’s Talking About

While everyone’s been watching oil, freight, and geopolitical risk, corrugated packaging has been quietly resetting its price floor.

Containerboard prices in North America are up roughly $100 per ton year-to-date, with a second wave of increases landing in June. That number matters more than it looks, because packaging touches almost every manufacturer. You ship in corrugated, you receive in corrugated, or your suppliers do.

The reason for the increase isn’t a demand spike. It’s supply. North American producers pulled nearly 10% of containerboard production capacity out of the market during 2025, with the last closures hitting in Q1 2026. Operating rates are now running in the low-to-mid 90% range, and that capacity isn’t coming back. Add rising wages, electricity costs, health insurance expenses, capital equipment costs, and tight fiber supply, and there’s no real relief in sight.

The question for H2 is how much more inflation your suppliers still need to recover, not whether box costs are rising.

The Structural Inflation Hiding Behind the Hormuz Headlines

Here’s the risk: procurement teams that fixate on Hormuz can miss cost pressures running on entirely separate timelines. Three deserve direct attention.

Labor. Manufacturing unit labor costs are up 3.4% year-over-year, and hourly compensation is climbing even faster. Manufacturers are getting more productive. They’re also paying significantly more per worker. If you’re buying fabricated components, machined parts, assemblies, or labor-intensive services, supplier price increase requests are a math problem instead of a negotiation tactic.

Electricity. Average electricity costs for U.S. manufacturers are up roughly 41% since 2021, and the forecasts point higher over the next decade. And it isn’t a one-line item. It sits underneath forging, casting, heat treatment, electroplating, and injection molding simultaneously. Add the AI data center buildout pulling harder on the grid than generation capacity can match, and electricity has become a strategic cost driver in its own right. Oil prices moderating won’t fix this one.

Plastic resins. Stage 2 intermediate demand prices for resins just hit the highest annual increase ever recorded. Domestic natural gas gives some insulation from global energy shocks, but resin pricing is still exposed to electricity costs, freight, chemical processing inputs, and labor. Hormuz reopening doesn’t touch most of that.

The Cost Stack Is Compounding — Not Stacking in Isolation

The real risk isn’t any single cost line. It’s that none of these pressures are isolated. They compound, and they land on your suppliers before they land on you.

A packaging supplier is absorbing higher containerboard, labor, and electricity costs at the same time. A domestic fabricator is absorbing higher labor, energy, and freight costs at the same time. A resin supplier is absorbing higher processing, utility, and transportation costs at the same time. Eventually, all of it surfaces at once, and procurement teams that were only tracking the geopolitical headline get blindsided by the structural inputs that built up underneath it.

Hormuz Is Improving. It Isn’t Normal Yet.

The MOU is meaningful progress. The diplomatic stage is done, and physical normalization has started. Commercial normalization hasn’t arrived. Daily vessel volumes are still well below pre-conflict levels. War-risk premiums are still elevated. Shipping executives are warning that backlogs will take weeks to clear.

And one major variable is still unresolved: the agreement guarantees toll-free passage through Hormuz for sixty days. After that, negotiations start over on who administers the Strait going forward. That means one of the biggest inputs into freight costs beyond late summer is still unknown.

Don’t assume full normalization just because an agreement got signed. Model both scenarios — toll-free normalization and a persistent Hormuz risk premium — until commercial conditions actually catch up to the diplomatic ones.

The Metals Timeline Is Longer Than the Headlines Suggest

There’s a similar lag building in metals. The sulphur supply disruptions that pushed up nickel, stainless steel, and copper costs are starting to reverse. But cost recovery doesn’t move at headline speed. Physical flows resume first. Production recovers next. Commodity markets adjust after that. Supplier pricing mechanisms follow last.

For stainless steel buyers, August pricing is largely locked in using pre-deal cost assumptions. September is the earliest point where normalization might meaningfully show up in surcharges. Copper could take longer still. The MOU changes the direction of travel — it doesn’t reverse the pricing that’s already in motion. (For a fuller breakdown of where copper, nickel, aluminum, and steel are headed independent of Hormuz, see our Industrial Metals Outlook 2026.)

What Procurement Teams Should Be Doing Right Now

Revisit your packaging assumptions. Packaging inflation isn’t temporary anymore. Review contracts and cost models with that as the baseline, not the exception.

Get ready for supplier conversations. Plenty of suppliers have been absorbing structural inflation for months without passing it on. Expect those conversations to accelerate through Q3, and expect them to come in clusters, not one at a time.

Separate structural costs from temporary costs. Energy-related premiums may ease as freight and oil normalize. Labor, electricity, and packaging costs likely won’t. Negotiate these separately. Bundling them into one conversation gives suppliers cover to hold the line on everything. (This is exactly the kind of contract-level distinction that belongs in your RFQ structure — see How to Run a Direct Materials RFQ for how to build escalation and index language in before you need it, not after.)

Use this window while it’s open. As energy and freight conditions ease, suppliers may be more willing to talk pricing structure than they were three months ago. That’s a real opening to lock in index-linked mechanisms and more transparent cost models before the next disruption cycle starts.

The Bottom Line

The Strait is opening. That’s genuinely good news. But reopening Hormuz doesn’t restore the cost structure of 2024, and treating it like it does is the fastest way to get caught flat-footed in Q3 supplier conversations.

Containerboard costs have reset. Labor costs are elevated. Electricity costs are climbing. Plastic resins are at record inflation. None of that started in February, and none of it ends when Hormuz normalizes.

The procurement teams that come out ahead over the next six months won’t be the ones celebrating the headline. They’ll be the ones who used the improving geopolitical picture as cover to finally address the structural inflation that’s been building underneath it the whole time.