Most manufacturing procurement teams are sourcing reactively without realizing it.

A supplier sends a price increase letter and procurement responds. A plant requests a new supplier and procurement evaluates one option. A shortage forces an emergency qualification and whoever can deliver gets the business. Each decision is made in isolation, optimized for the immediate problem, with no view into how it connects to the broader category.

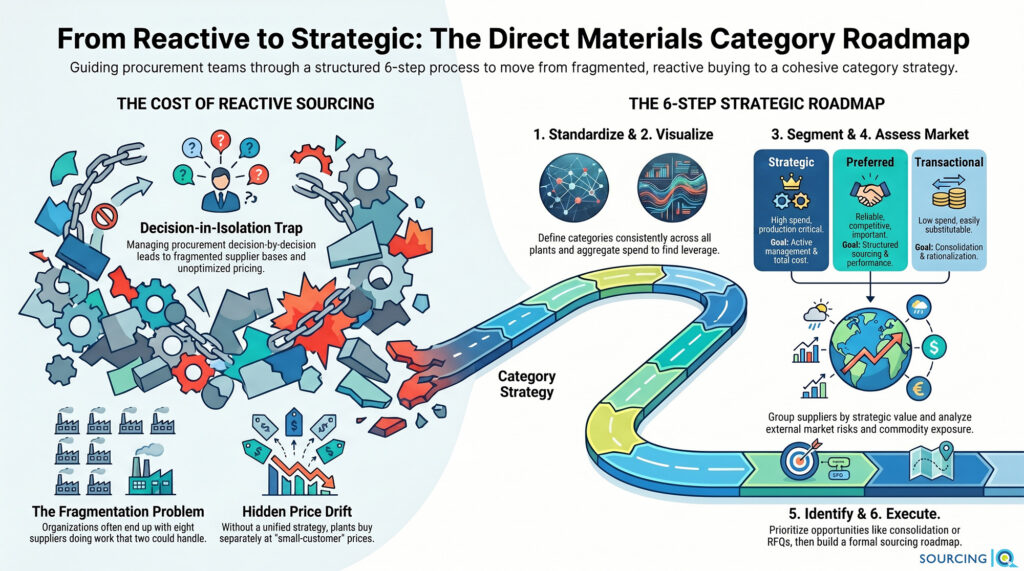

This is how supplier bases get fragmented. It’s how pricing drifts upward without anyone noticing. It’s how the organization ends up with eight suppliers doing work that two could handle, each buying separately at small-customer prices.

Category strategy is the structural fix. Instead of managing procurement decision-by-decision, it organizes sourcing around coherent spend groups with defined analysis, supplier segmentation, market awareness, and a sourcing roadmap that creates repeatable outcomes.

Here’s how a category strategy actually built.

Step 1 — Define the Category Clearly

Before any analysis begins, the category needs a clean definition. This is less obvious than it sounds.

In most manufacturing organizations, similar components are classified differently across plants, ERP systems, and buyers. One facility calls them “precision machined components.” Another calls them “CNC parts.” A third has them scattered across a dozen part-number-level line items with no common grouping. Aggregating spend across those inconsistencies without first standardizing the category definition produces unreliable analysis. And unreliable analysis produces bad sourcing decisions.

A well-defined category groups materials that share similar sourcing dynamics, supplier markets, or manufacturing processes. Typical direct materials categories in manufacturing:

- Machined components (aluminum, steel, complex assemblies)

- Castings and forgings

- Fabricated metal assemblies

- Plastics and molded components

- Electronics and electrical assemblies

- Packaging

The category boundaries don’t need to be perfect. They need to be consistent. Once the same classification is applied across plants and systems, the analytical picture becomes reliable. Until then, every analysis built on top of it is suspect.

Effective category management requires market intelligence, supplier strategy, and disciplined execution. We can help.

Step 2 — Build Spend Visibility Within the Category

After the category is defined, the next step is understanding how spend is actually distributed inside it.

This means pulling and analyzing:

- Total category spend, consolidated across all plants and business units

- Supplier concentration: how many suppliers, what share of spend each carry, and whether that distribution reflects a deliberate strategy or organic accumulation

- Plant-level purchasing patterns: are all plants sourcing this category, or is it concentrated in certain facilities?

- Pricing variation: are similar components carrying similar prices, or is there meaningful variance across plants or suppliers?

- Sourcing history: when was this category last competitively sourced? Are any contracts approaching renewal?

What tends to surface at this step: the category is more fragmented than anyone suspected. Multiple plants are buying similar components from different suppliers, each negotiating as a small customer without visibility into what anyone else is doing. That fragmentation is both the problem and the opportunity.

Spend visibility doesn’t need to be perfect to be useful. It needs to be accurate enough to answer: who are we buying from, what are we spending, and where is the leverage concentrated?

Step 3 — Segment Suppliers Within the Category

Not all suppliers in a category deserve the same level of procurement attention. Supplier segmentation creates the clarity that allows procurement energy to be directed appropriately.

A practical segmentation for direct materials categories:

Strategic suppliers. High spend, specialized capability, or production-critical relationship. These suppliers require active management: regular performance reviews, collaborative improvement initiatives, commercial terms that reflect their importance and your dependence. The goal with strategic suppliers is total cost which includes performance and continuity.

Preferred suppliers. Reliable, commercially competitive, important to operations but not uniquely specialized. These are the relationships where structured sourcing events and performance management create the most straightforward value.

Transactional suppliers. Lower spend, easily substitutable, minimal strategic importance. These are candidates for consolidation or rationalization . The energy spent managing twenty transactional suppliers is better directed toward fewer, more strategic relationships.

High-risk suppliers. May not be high-spend, but supply risk makes them disproportionately important. Sole or single sources for critical components, suppliers with capacity constraints, or suppliers with performance history that suggests reliability problems. These are high-touch and require contingency planning regardless of spend level.

Segmentation prevents the most common misallocation of procurement effort: spending disproportionate time on transactional suppliers while strategic relationships run on autopilot.

Step 4 — Assess Market Dynamics and Supply Risk

Category strategy that only looks inward at spend and suppliers is missing half the picture. The supply market context determines what’s achievable and how aggressive a sourcing approach makes sense.

Assess:

Supplier market structure. Are there five qualified suppliers who actively compete for business, or two — one of whom is dominant? Competitive market dynamics change what a structured RFQ can realistically deliver.

Commodity exposure. Is pricing in this category largely driven by raw material inputs like steel, aluminum, resins, copper? If so, how are those inputs trending and how is that movement reflected in current supplier pricing?

Geographic concentration. Is the supplier base clustered in a specific region, creating exposure to logistics disruption, tariff changes, or labor market conditions that affect multiple suppliers simultaneously?

Lead time and capacity dynamics. Are suppliers running near capacity? Are lead times extending across the category? Capacity-constrained markets affect consolidation decision. If the supplier base can’t absorb additional volume, consolidation creates more risk than it eliminates.

Qualification barriers. How long does it take to qualify a new supplier in this category? If qualification involves engineering approval, PPAP, or customer notification, switching costs are real, and aggressive consolidation strategies may underperform because the implementation is harder than the analysis suggested.

Market awareness grounds a category strategy by preventing sourcing plans that look compelling on a spreadsheet from failing on contact with operational reality.

Step 5 — Identify Sourcing Opportunities

With spend visible, suppliers segmented, and market dynamics understood, the category picture is clear enough to identify where value actually exists.

Common opportunities in direct materials categories:

Supplier consolidation. Where fragmented spend can be aggregated into fewer, more strategically managed relationships (subject to the qualification and capacity constraints identified in Step 4).

Competitive RFQs. Categories where pricing hasn’t been tested recently and the supplier market supports real competition. This is the most straightforward lever, and often the most underutilized.

Cross-plant pricing alignment. Closing the pricing gap when the same or similar components carry different prices at different facilities either by renegotiating with existing suppliers or by establishing enterprise-level pricing expectations.

Specification standardization. Opportunities to reduce unnecessary variation in component specs across plants or programs, which opens the door to aggregation and simplifies supplier management. This one requires engineering partnership, but the procurement team’s job is to quantify the cost driver and bring it to the conversation.

Dual sourcing or supplier development. Where single-source concentration creates unacceptable risk, developing a qualified alternative — even for partial volume — provides operational insurance and commercial leverage simultaneously.

Prioritize opportunities by sequencing: what’s most impactful, and what’s most feasible to execute given qualification requirements, organizational bandwidth, and timing constraints? The best category strategy executes in waves, not all at once.

Step 6 — Build the Category Sourcing Plan

The sourcing plan converts category analysis into a structured execution roadmap. This is the document that turns strategy from a conversation into a schedule.

A practical category sourcing plan covers:

- Sourcing priorities: Which initiatives are being pursued, in what order, and why

- Target suppliers: Who gets invited to what events, and what the supplier base looks like post-execution

- Timing: When each initiative launches, what the milestones are, and when implementation is expected to complete

- Expected outcomes: Realistic savings estimates, working capital improvements, risk reductions, or performance improvements tied to each initiative

- Ownership: Who is responsible for each element including (and especially) the parts that happen after award

The sourcing plan does two things simultaneously: it makes execution concrete and it creates alignment across procurement, operations, and engineering. When everyone can see what’s being worked on and why, the cross-functional coordination that complex category changes require becomes significantly easier to achieve.

Step 7 — Monitor and Evolve the Strategy

Category strategy is not a document you write once and frame on the wall. The supply market changes. Commodity prices move. Suppliers’ capabilities and capacity shift. Demand patterns evolve. A strategy that reflected market reality when it was written may be obsolete twelve months later.

Effective category management builds in ongoing review:

- Track actual sourcing outcomes against plan: what was expected, what was achieved, what was different

- Monitor supplier performance against established expectations, not just in response to problems

- Watch for market developments that change the competitive landscape or cost structure

- Identify new opportunities that emerge as spend patterns shift or new suppliers enter the market

The cadence doesn’t need to be intense: quarterly reviews of major categories, semi-annual reviews of stable ones. What matters is that the category strategy stays current and decision-ready rather than becoming a historical artifact that nobody references.

Category Strategy Creates Procurement Discipline

The shift from transactional procurement to category-based sourcing is the clearest indicator that a procurement function is maturing. It’s what turns isolated sourcing events into a systematic, repeatable capability.

Without category strategy, procurement manages individual transactions and responds to individual problems. With it, procurement makes deliberate decisions about the supply base, executes structured sourcing on a defined cadence, and builds institutional knowledge that compounds over time.

For mid-market manufacturers trying to sustain sourcing savings, not just capture them once, category strategy is the operational mechanism that makes it possible.